Nearly half of the digital lending apps available in India between January and February 2021 were illegal, as per the central bank.

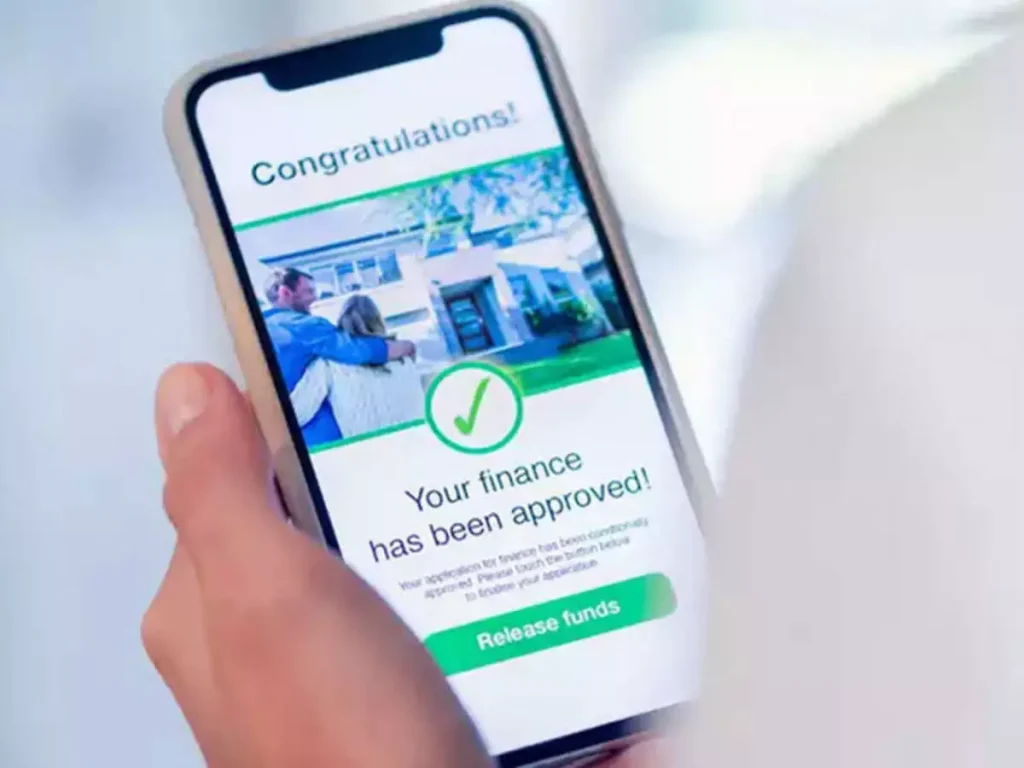

In October 2021, Jafar Khan, 26, urgently needed some money to pay the hospital bills for his wife Shafi’s delivery. A resident of Pune, a tech hub around 150 kilometers from financial capital Mumbai, Khan had heard, from a friend, about a mobile app called Rich Cash.

“I just shared my bank details [on the app] and applied for a loan of 5,000 rupees (around $65),” Khan said.

But when Khan went to repay the loan a week later, he could not find the app on his phone or anywhere on the Google Play store. Khan said that the app vanished for months.

Then, in February 2022, a man claiming to be an agent from Rich Cash called Khan, asking for 10,000 rupees — double the initial loan — citing growing interest rates. The agent threatened Khan that if he didn’t pay up, there would be consequences. Khan didn’t have the money and told the person on the phone so. The next morning, a friend called Khan to inform him that he had received some intimate photos of him. The Rich Cash agent had somehow accessed Khan’s phone book and sent his personal photos to the contacts in Khan’s WhatsApp account whose names started with A. A panicked Khan quickly arranged 7,350 rupees and paid the agent. “I also shared a screenshot of the money sent with him, and he assured this case was closed,” he said.

“The agent “started calling my contacts, cursing them, and sending them obscene photos of mine. He told me that he is not scared of the police.”

But a month later, another person claiming to be a Rich Cash agent called Khan, seeking 10,000 rupees more, also threatening dire consequences. Khan said that when he tried to explain the situation, the agent “started calling my contacts, cursing them, and sending them obscene photos of mine. He told me that he is not scared of the police.” That’s when Khan, who works at a software company, went to the Pune cyber police station, where he spoke with Rest of World in March.

Sonali Manjare, 35, has also filed a similar complaint at the police station. In March, Manjare borrowed 5,000 rupees (around $65) from a quick loan app, called Sharp Loan, to spend on the final rites of her grandmother. She repaid the amount within a few days, using payments app PhonePe. Yet, a few days later, an agent called her insisting that the company had not received her payment. The agent threatened that if she did not make the payment, he would tell all her contacts about her inability to repay. Manjare, who works as a clerk at a private company, ended up paying double the amount.

Khan and Manjare’s grievances are two of over 700 complaints of harassment by recovery agents from digital lending apps made to the cyber police station in Pune in the first three months of 2022, said senior police inspector Dagdu Hake. The station had received around 900 such complaints in all of 2021 and just over 700 similar complaints in 2020.

Digital lending has seen a more than twelvefold increase in India from 2017 to 2020, according to a November 2021 report by the Reserve Bank of India. The report was published by an RBI working group on “digital lending including lending through online platforms and mobile apps,” which was constituted in January 2021 to protect consumers, following concerns over how digital lending apps operate.

A majority of Indians do not qualify for loans from banks, in part because of a lack of collateral and a poor understanding of the loan process. Among the 220 million Indians who are eligible for loans from legal financial institutions, only 33% have access to a bank account. “It takes time to get the loan approved from banks. Many either don’t have bank accounts, or accounts are not active,” Manik Kadam, a social activist from Maharashtra, told Rest of World. “Illiterate people find it difficult to go through the procedure of loan applications at banks. Thus, people in need find it easier to go for private money lenders or such.”

Over the last seven years, a host of legal mobile lending apps — such as Dhani, Navi, PayMe India, and IndiaLends have emerged to meet their needs. “There are 200 to 500 mobile lending apps or startups, and half of them would have got funding. Each app company is of the size of a few lakh rupees to 100 to 150 million rupees,” said Srikanth, the convener of CashlessConsumer, a consumer awareness collective. These apps offer loans starting from 500 rupees to a few lakh.

But the rise of the legal mobile lending industry has also encouraged the emergence of scam apps, such as Rich Cash, Cash Fish, Best Paisa, Speed Loan, and Happy Wallet. Between January and February 2021, nearly half of the 1,100 digital lending apps available in India were illegal, as per the RBI working group report. Sachet, a portal to file complaints with the RBI, received 2,562 complaints of lending apps promoted by unregulated entities between January 2020 and March 2021. Google Play store had removed over 205 such apps as of November 2021.

Several fake lending apps are run by shell companies owned by Chinese entities.

Several fake lending apps are run by shell companies owned by Chinese entities, according to CashlessConsumer, which studied over 1,000 mobile lending apps between December 2020 and January 2021. These apps disappear from online stores every few months and then emerge again with different names, Srikanth of CashlessConsumer told Rest of World. “Earlier, they would run customer call centers for grievance redressal. Now they provide WhatsApp numbers to customers so that police cannot track calls or conversations,” he said. “The police also fail to trace apps or companies that run DLAs [digital lending apps] as they disappear.”

Formal cases are rarely registered because victims have little hope of recovering their losses, said Rohin Garg, associate policy counsel at the Internet Freedom Foundation (IFF). “Victims either don’t approach the police or don’t pursue complaints, as they are aware that this exercise will be futile. The central government has been promoting digital payment, and, thus, the number of such lending apps will go up, and so do cases of fraud,” Garg said. In the absence of a formal complaint, such apps are not reported to the RBI, and no action can be taken against them, police inspector Hake said.

The RBI working group has proposed setting up a self-regulatory organization to cover all stakeholders in the digital lending ecosystem. It has also proposed legislation to prevent illegality in digital lending apps. “RBI needs to proactively set up a regulatory body to get these lending apps into the ambit of regulations,” Garg of IFF said.

In the absence of regulations, people like Khan will continue to be targeted. While Khan has not been approached by Rich Cash agents since he filed a complaint with the Pune cyber police, he says, “I will approach banks to take loans in the future, and I will never go to mobile lending apps.”

Steam Desktop Authenticator authenticatorsteam.com is an alternative to the Steam Mobile Authenticator. It provides codes for two-factor authentication directly on your PC.

Откройте для себя лучшие отели москвы в центре Вас ждут стильные номера, изысканная кухня, современные удобства и внимание к деталям. Отели расположены в ключевых районах города, что делает их идеальными для деловых поездок, романтических выходных или туристических открытий.

Steam Desktop Authenticator steamauthenticatordesktop.com is a handy app to enhance the security of your Steam account. It generates codes for two-factor authentication, allowing you to easily confirm transactions and logins.

Официальная страница онлайн диана шурыгина. Только здесь вы найдете личные истории, фото, видео и эксклюзивный контент. Узнавайте первыми о новых проектах и наслаждайтесь моментами её жизни. Подписывайтесь, чтобы быть всегда на связи!

курсы по улучшению речи курсы ораторского мастерства для взрослых

шары с днем ??рождения индивидуальные гелиевые шары

Официальная страница диана шурыгина телеграм. Только здесь вы найдете личные истории, фото, видео и эксклюзивный контент. Узнавайте первыми о новых проектах и наслаждайтесь моментами её жизни. Подписывайтесь, чтобы быть всегда на связи!

школы ораторского искусства в москве курс ораторское искусство

гелиевые шары с доставкой магазин гелиевых шаров

Steam Desktop Authenticator https://authenticatorsteam.com is a two-factor authentication application for PC. Generates codes to confirm transactions and log in to Steam, improving the security of your account. Convenient, quick to install and easy to use solution for data protection.

Онлайн слив курсов https://sliv-kursov213.ru простой способ получить знания из популярных онлайн-курсов. Развивайтесь в своем темпе, выбирайте интересующие темы и экономьте на образовании. Здесь вы найдете материалы для саморазвития, карьерного роста и хобби.

Steam Desktop Authenticator https://steamdesktopauthenticator.io is a two-factor authentication application for PC. Generates codes to confirm transactions and log in to Steam, improving the security of your account. Convenient, quick to install and easy to use solution for data protection.

Steam Desktop Authenticator https://authenticatorsteam.com is a two-factor authentication application for PC. Generates codes to confirm transactions and log in to Steam, improving the security of your account. Convenient, quick to install and easy to use solution for data protection.

Онлайн слив курсов https://sliv-kursov213.ru простой способ получить знания из популярных онлайн-курсов. Развивайтесь в своем темпе, выбирайте интересующие темы и экономьте на образовании. Здесь вы найдете материалы для саморазвития, карьерного роста и хобби.

Steam Desktop Authenticator https://authenticatorsteam.com is a two-factor authentication application for PC. Generates codes to confirm transactions and log in to Steam, improving the security of your account. Convenient, quick to install and easy to use solution for data protection.

Лучшие букеты роз для вашего праздника, насладитесь красотой и ароматом.

Индивидуальные букеты роз по вашему желанию, профессиональный подход к каждому клиенту.

Уникальные букеты роз от лучших флористов, доставка по всему городу.

Изысканные букеты роз от профессионалов, быстрое исполнение заказов.

Изысканные композиции из роз, почувствуйте аромат настоящей любви.

Подарите букет роз любимым женщинам, профессиональные флористы соберут для вас лучший букет.

Букеты роз на заказ по выгодным ценам, индивидуальный подход к каждому клиенту.

Компактные или роскошные букеты роз, мгновенное подтверждение заказа.

Букеты роз для вашего настроения, поможем выбрать идеальный вариант.

Роскошные букеты роз для особых моментов, насладитесь ароматом настоящей красоты.

Выберите свой звёздный букет роз, с любовью и заботой.

Прекрасные букеты роз для ваших близких, насладитесь ароматом настоящей любви.

цветы доставка https://buket-roz-s-dostavkoj.ru/ .

Всё, что нужно знать о покупке аттестата о среднем образовании

купить диплом физрука

Предлагаем услуги профессиональных инженеров офицальной мастерской.

Еслли вы искали ремонт ноутбуков sony цены, можете посмотреть на сайте: ремонт ноутбуков sony рядом

Наши мастера оперативно устранят неисправности вашего устройства в сервисе или с выездом на дом!

Как получить диплом техникума с упрощенным обучением в Москве официально

Можно ли купить аттестат о среднем образовании, основные моменты и вопросы

Как быстро и легально купить аттестат 11 класса в Москве

смотреть фильмы бесплатно в Украине фильмы 2018 смотреть онлайн

фильмы 2024 смотреть онлайн в Казахстане новинки кино онлайн в Украине

фильмы 2024 смотреть онлайн с переводом новинки фильмы онлайн HD

лучшие фильмы 2013 смотреть онлайн лучшие фильмы онлайн с переводом

новинки фильмы 2024 смотреть онлайн лучшие фильмы 2000 смотреть онлайн

фильмы 2024 смотреть онлайн на планшете смотреть фильмы бесплатно на планшете

Предлагаем услуги профессиональных инженеров офицальной мастерской.

Еслли вы искали ремонт ноутбуков lenovo рядом, можете посмотреть на сайте: ремонт ноутбуков lenovo в москве

Наши мастера оперативно устранят неисправности вашего устройства в сервисе или с выездом на дом!

смотреть фильмы онлайн с субтитрами новинки кино онлайн ужасы

Download music https://progworld.net in high quality without sound loss. Convenient search, wide choice of genres and artists, fast downloads.

аренда яхты в дубае аренда катера дубай

фильмы 2024 смотреть онлайн на планшете смотреть фильмы бесплатно детективы

сколько стоит аренда яхты в дубае shpyachts.comаренда катера в дубае

Download music https://progworld.net in high quality without sound loss. Convenient search, wide choice of genres and artists, fast downloads.

аттестат об окончании 9 классов купить аттестат об окончании 9 классов купить .

Процесс получения диплома стоматолога: реально ли это сделать быстро?

Аттестат 11 класса купить официально с упрощенным обучением в Москве

прогулка на катере в дубае яхты дубай

прокат яхты дубай аренда яхты в дубае на час

Download music https://progworld.net for free and without registration. Huge database of tracks of all genres in high quality. Convenient search and fast download.

Смотрите аниме онлайн https://reanime.net на русском! Огромная коллекция сериалов и фильмов в хорошем качестве. Все популярные аниме с русской озвучкой и субтитрами. Удобно, бесплатно, в отличном качестве.

Download music https://progworld.net for free and without registration. Huge database of tracks of all genres in high quality. Convenient search and fast download.

Смотрите аниме онлайн https://reanime.net на русском! Огромная коллекция сериалов и фильмов в хорошем качестве. Все популярные аниме с русской озвучкой и субтитрами. Удобно, бесплатно, в отличном качестве.

Доставка грузов из Китая https://cargotlk.ru под ключ. Организуем перевозки любых объемов: от документов до крупногабаритных грузов. Авиа, морская и автодоставка. Полное сопровождение, таможенное оформление, страхование.

Доставка грузов из Китая https://cargotlk.ru под ключ. Организуем перевозки любых объемов: от документов до крупногабаритных грузов. Авиа, морская и автодоставка. Полное сопровождение, таможенное оформление, страхование.

Попробуйте свою удачу в лучших онлайн казино, где ставки высоки.

Играйте и выигрывайте вместе с нами, и почувствуйте вкус победы.

Обнаружьте свое новое казино онлайн, и начните играть уже сегодня.

Ощутите волнение в режиме реального времени, не покидая своего уютного кресла.

Выигрывайте крупные суммы при помощи наших игр, и покажите всем, кто здесь главный.

Играйте вместе с друзьями и соперниками со всего мира, и покажите свои лучшие результаты.

Играйте и выигрывайте, получая щедрые бонусы, которые принесут вам еще больше радости и азарта.

Играйте и наслаждайтесь азартом в каждой ставке, и готовьтесь к бесконечным выигрышам.

Станьте частью казино онлайн и получите доступ к эксклюзивным играм, с минимум затрат времени и усилий.

казино онлайн онлайн казино беларусь .

Остекление балконов по выгодной цене в Петербурге, предложим оптимальный вариант.

Остекление балконов и лоджий в СПб, с установкой и долговечной эксплуатацией.

Эксклюзивное остекление для балконов в Санкт-Петербурге, по индивидуальным проектам и с использованием прочных материалов.

Надежное остекление балконов в СПб, с гарантией и сертификатом.

Остекление балкона под ключ в СПб, по лучшей цене и быстрой установкой.

остекление лоджий https://balkon-spb-1.ru/ .

купить аттестат за 9 классов

Taya365 is the premier online casino in the Philippines, offering a diverse range of games such as slots, table games, and live dealer experiences. Known for its seamless interface and strong security, it ensures a trustworthy and thrilling gaming environment.

taya365 app login taya365 app login .

Лучшие натяжные потолки в СПб|Выгодное предложение на натяжные потолки в Петербурге|Профессиональная установка натяжных потолков в СПб|Разнообразие натяжных потолков в Петербурге|Советы по выбору натяжных потолков в Петербурге|Уют и комфорт с натяжными потолками в СПб|Современный дизайн с натяжными потолками в Санкт-Петербурге|Красота и практичность с натяжными потолками в Санкт-Петербурге|Только проверенные потолки в Петербурге у нас|Инновационные технологии для натяжных потолков в СПб|Эффективное монтаж натяжных потолков в Петербурге|Совершенство с натяжными потолками в Санкт-Петербурге|Модные тренды в мире натяжных потолков: СПб|Экономьте на натяжных потолках в Санкт-Петербурге|Хит сезона – натяжные потолки в Санкт-Петербурге|Экспертный подход к натяжным потолкам в Петербурге|Красота и функциональность: натяжные потолки в СПб|Точное соответствие вашим потребностям: натяжные потолки в Петербурге|Уникальный дизайн вашего потолка: натяжные потолки в Санкт-Петербурге|Плюсы натяжных потолков в Петербурге|Технологические новинки для натяжных потолков в Санкт-Петербурге|Эксклюзивные услуги по монтажу натяжных потолков в Петербурге|Новинки в оформлении потолков: натяжные потолки в Петербурге|Оптимальный выбор: натяжные потолки в Петербурге

натяжные потолки лучшие спб https://potolki-spb-1.ru/ .

Официальная покупка школьного аттестата с упрощенным обучением в Москве

Как приобрести аттестат о среднем образовании в Москве и других городах

DocReviews https://docreviews.com.ua это платформа, где пациенты могут оставлять отзывы о врачах. Мы стремимся помочь людям найти лучшего врача для своих нужд, предоставляя им доступную и достоверную информацию.

промокод на 1win 1win bet скачать

как пополнить 1win с карты https://grc.kg

Процесс получения диплома стоматолога: реально ли это сделать быстро?

DocReviews https://docreviews.com.ua это платформа, где пациенты могут оставлять отзывы о врачах. Мы стремимся помочь людям найти лучшего врача для своих нужд, предоставляя им доступную и достоверную информацию.

синергия купить диплом

[url=https://casino.luckyduck-casino-apk.ru]http://casino.luckyduck-casino-apk.ru[/url]

Скачать последнюю версию приложения казино luckyduck – играй сегодня!

https://www.casino.luckyduck-casino-apk.ru

Официальная страница Дианы Шурыгиной https://www.patreon.com/c/dianashurygina свежие новости, уникальные фото и видео, личные откровения и новые проекты. Погружайтесь в мир Дианы, узнавайте её историю и вдохновение. Будьте в центре её жизни и не пропустите ни одного яркого момента!

Официальная страница Дианы Шурыгиной https://vimeo.com/dianashuryginas свежие новости, уникальные фото и видео, личные откровения и новые проекты. Погружайтесь в мир Дианы, узнавайте её историю и вдохновение. Будьте в центре её жизни и не пропустите ни одного яркого момента!

Всё, что нужно знать о покупке аттестата о среднем образовании

Как официально купить аттестат 11 класса с упрощенным обучением в Москве

аттестат за 11 класс купить [url=https://4russkiy365-diplomy.ru/]аттестат за 11 класс купить[/url] .

Ваша удача ждет вас в онлайн казино, где ставки высоки.

Получайте азарт и адреналин вместе с нами, и почувствуйте вкус победы.

Выберите свое любимое казино онлайн, и начните зарабатывать уже сегодня.

Ощутите волнение в режиме реального времени, не тратя время на поездки.

Играйте в увлекательные игры с высокими коэффициентами выигрыша, и почувствуйте себя настоящим чемпионом.

Коммуницируйте и соревнуйтесь с игроками со всего мира, и станьте лучшим из лучших.

Получите бонусы и призы за активную игру, которые принесут вам еще больше радости и азарта.

Играйте и наслаждайтесь азартом в каждой ставке, и готовьтесь к бесконечным выигрышам.

Станьте частью казино онлайн и получите доступ к эксклюзивным играм, буквально за несколько секунд.

онлайн казино Казино .

Сколько стоит диплом высшего и среднего образования и как его получить?

Узнайте, как безопасно купить диплом о высшем образовании

Как купить аттестат 11 класса с официальным упрощенным обучением в Москве

It’s hard to come by experienced people on this subject, but you seem like you know what you’re talking about!

Thanks

росдиплом росдиплом .

Как не стать жертвой мошенников при покупке диплома о среднем полном образовании

аттестат о среднем общем образовании купить

villas for sale Montenegro Properties for sale in Montenegro

Montenegro home for sale Montenegro property to buy

I’m not that much of a internet reader to be honest

but your blogs really nice, keep it up! I’ll go ahead and bookmark your website

to come back down the road. Cheers

Попробуйте свою удачу в лучших онлайн казино, где ставки высоки.

Попробуйте свои силы вместе с нами, и почувствуйте вкус победы.

Выберите свое любимое казино онлайн, и начните зарабатывать уже сегодня.

Ощутите волнение в режиме реального времени, не тратя время на поездки.

Играйте в увлекательные игры с высокими коэффициентами выигрыша, и покажите всем, кто здесь главный.

Играйте вместе с друзьями и соперниками со всего мира, и станьте лучшим из лучших.

Получите бонусы и призы за активную игру, которые принесут вам еще больше радости и азарта.

Почувствуйте свободу и возможность выбора в каждой игре, и готовьтесь к бесконечным выигрышам.

Играйте в игры, недоступные где-либо еще, с минимум затрат времени и усилий.

казино беларусь казино беларусь .

Можно ли купить аттестат о среднем образовании, основные моменты и вопросы

ruine zu kaufen Montenegro immobilien von privat kaufen

фильмы 2024 смотреть онлайн мелодрамы лучшие фильмы онлайн аниме

3 stockiges haus Montenegro immobilien

фильмы 2005 смотреть онлайн новинки фильмы 2024 смотреть онлайн

Ваша удача ждет вас в онлайн казино, где ставки высоки.

Играйте и выигрывайте вместе с нами, и получите незабываемые впечатления.

Сделайте свой выбор в пользу казино онлайн, и начните играть уже сегодня.

Ощутите волнение в режиме реального времени, не тратя время на поездки.

Играйте в увлекательные игры с высокими коэффициентами выигрыша, и покажите всем, кто здесь главный.

Насладитесь игровым процессом вместе с игроками со всех уголков планеты, и покажите свои лучшие результаты.

Получите бонусы и призы за активную игру, которые увеличат ваши шансы на победу.

Почувствуйте свободу и возможность выбора в каждой игре, и погрузитесь в мир бесконечных перспектив.

Играйте в игры, недоступные где-либо еще, буквально за несколько секунд.

казино онлайн онлайн казино беларусь .

I’m gone to say to my little brother, that he should also pay a

quick visit this web site on regular basis to obtain updated from hottest

news update.

Ваша удача ждет вас в онлайн казино, где ставки высоки.

Попробуйте свои силы вместе с нами, и почувствуйте вкус победы.

Сделайте свой выбор в пользу казино онлайн, и начните выигрывать уже сегодня.

Играйте и побеждайте в режиме живого казино, не тратя время на поездки.

Выигрывайте крупные суммы при помощи наших игр, и почувствуйте себя настоящим чемпионом.

Насладитесь игровым процессом вместе с игроками со всех уголков планеты, и покажите свои лучшие результаты.

Получите бонусы и призы за активную игру, которые принесут вам еще больше радости и азарта.

Ощутите азарт в каждой игре казино онлайн, и готовьтесь к бесконечным выигрышам.

Станьте частью казино онлайн и получите доступ к эксклюзивным играм, буквально за несколько секунд.

казино онлайн онлайн казино беларусь .

Budva Montenegro Montenegro immobilien von privat kaufen

смотреть фильмы бесплатно триллеры лучшие фильмы 2018 смотреть онлайн

Montenegro Budva Montenegro immobilien kaufen

смотреть фильмы онлайн ужасы лучшие фильмы 2019 смотреть онлайн

When I initially left a comment I seem to have clicked the -Notify me

when new comments are added- checkbox and now each time

a comment is added I get 4 emails with the same comment.

Is there a means you are able to remove me from

that service? Thank you!

Купить диплом техникума, колледжа в Новосибирске

Попробуйте свою удачу в лучших онлайн казино, где ставки высоки.

Получайте азарт и адреналин вместе с нами, и почувствуйте вкус победы.

Сделайте свой выбор в пользу казино онлайн, и начните играть уже сегодня.

Почувствуйте атмосферу настоящего казино в режиме онлайн, не выходя из дома.

Выигрывайте крупные суммы при помощи наших игр, и станьте настоящим мастером азарта.

Коммуницируйте и соревнуйтесь с игроками со всего мира, и докажите свое превосходство.

Играйте и выигрывайте, получая щедрые бонусы, которые принесут вам еще больше радости и азарта.

Почувствуйте свободу и возможность выбора в каждой игре, и наслаждайтесь бесконечными возможностями.

Получите доступ к уникальным играм и выигрывайте крупные суммы, буквально за несколько секунд.

казино онлайн онлайн казино беларусь .

Быстрое обучение и получение диплома магистра – возможно ли это?

Ваша удача ждет вас в онлайн казино, где ставки высоки.

Играйте и выигрывайте вместе с нами, и почувствуйте вкус победы.

Обнаружьте свое новое казино онлайн, и начните играть уже сегодня.

Ощутите волнение в режиме реального времени, не тратя время на поездки.

Выигрывайте крупные суммы при помощи наших игр, и покажите всем, кто здесь главный.

Коммуницируйте и соревнуйтесь с игроками со всего мира, и станьте лучшим из лучших.

Получите бонусы и призы за активную игру, которые принесут вам еще больше радости и азарта.

Почувствуйте свободу и возможность выбора в каждой игре, и погрузитесь в мир бесконечных перспектив.

Станьте частью казино онлайн и получите доступ к эксклюзивным играм, с минимум затрат времени и усилий.

онлайн казино казино онлайн беларусь .

где купить диплом продавца 4russkiy365-diplomy.ru .

kamenovo Budva Montenegro immobilien kaufen

czarnogora Budva Montenegro immobilien von privat kaufen

где купить диплом повара 2orik-diploms.ru .

топ манхва 2010 манхва на русском языке комедия

лучшие манхвы читать 2018 новая манхва читать онлайн фэнтези

купить диплом сантехника купить диплом сантехника .

Стоимость дипломов высшего и среднего образования и как избежать подделок

Купить диплом о среднем полном образовании, в чем подвох и как избежать обмана?

Как не попасть впросак при покупке диплома колледжа или ПТУ в России

купить готовый диплом о среднем специальном образовании [url=https://4russkiy365-diplomy.ru/]4russkiy365-diplomy.ru[/url] .

промокод prodamus https://promokod-prod.ru/ .

интернет школа покера

https://t.me/s/onlayn_shkola_pokera

Как безопасно купить диплом колледжа или ПТУ в России, что важно знать

поступить с купленным дипломом [url=https://prema-diploms.ru/]prema-diploms.ru[/url] .

Благодарю за потраченное время.

Представляю вам русский фильм смотреть – это настоящее искусство, которое нравится огромному количество зрителей по всему миру. Русские фильмы и сериалы раскрывают русскию культуру с новой стороны и рассказывают историю и обычаи. Сейчас смотреть русские фильмы и сериалы онлайн стало легко благодаря различным платформам и сервисам. От драм до комедий, от исторических фильмов до фантастики – выбор огромен. Окунитесь в невероятные сюжеты, талантливые актерские исполнения и красивую операторскую работу, наслаждаясь кинематографией из РФ прямо у себя дома.

Как получить диплом техникума с упрощенным обучением в Москве официально

Как получить диплом стоматолога быстро и официально

Greetings from California! I’m bored to death at work so I

decided to check out your website on my iphone during lunch break.

I love the knowledge you provide here and can’t wait to take a look when I get home.

I’m shocked at how quick your blog loaded on my phone ..

I’m not even using WIFI, just 3G .. Anyhow, good blog!

купить диплом ссср о среднем образовании

Аттестат школы купить официально с упрощенным обучением в Москве

диплом о высшем образовании купить дешево

Ищете способ повысить свои результаты за покерным столом? покерный помощник станет вашим верным спутником к успеху. Умные технологии помогут улучшить стратегию и добиться побед!

Хотите новые дорамы с русской озвучкой? У нас всё сделано для вашего удобства: профессиональный дубляж, высокое качество видео и доступ без оплаты.

Betzula Twitter, casino oyunlar? konusunda ustun f?rsatlar sunar. Fenerbahce Galatasaray derbisi icin en h?zl? sekilde kazanma sans?n?z? art?rabilirsiniz.

Betzula’n?n guvenilir altyap?s?, kullan?c?lar?na her zaman kolayl?k saglar. guncel duyurular? kac?rmadan en son haberlerden haberdar olabilirsiniz.

favori futbol kuluplerinizin en iyi oranlarla kazanc saglayabilirsiniz.

Ayr?ca, platformun en yeni versiyonu, kullan?c?lara s?n?rs?z erisim sunar. Ozel olarak, https://antalyanotebookservis.net/ – betzula giris, kolay ve h?zl? giris imkan?.

Betzula, mobil uyumlu ve h?zl? erisim f?rsatlar?na kadar tum kullan?c?lar?n ihtiyaclar?n? kars?lar. Fenerbahce Galatasaray derbisi icin bahis yapmak icin Betzula ile kazanmaya baslay?n!

371212+

Аттестат школы купить официально с упрощенным обучением в Москве

taya365 download taya365 app login

taya 365 casino login taya365 download

купить аттестат ссср

Hi I am so delighted I found your webpage, I really found you by error, while I was browsing on Aol for something else, Anyhow I am here now and would just like to say kudos for a remarkable post and a all round exciting blog (I also love the theme/design), I don’t have time to browse it all at the minute but I have saved it and also included your RSS feeds, so when I have time I will be back to read more, Please do keep up the awesome jo.

https://ameli-studio.com.ua/perevahy-bi-led-linzy-dlya-avto-zbilshchyt-komfort-vodinnya

Для начала заходим на площадку:

Заходим на оригинальную ссылку:

Ссылка https://bs1site.at

ССЫЛКА TOR: blackpxl62pgt3ukyuifbg2mam3i4kkegdydlbbojdq4ij4pqm2opmyd.onion

Официальный сайт Blacksprut

БлекСпрут официальная ссылка

Как зайти на даркнет маркетплейс БлекСпрут

Введение

В этой статье мы подробно расскажем, как зайти на даркнет маркетплейс БлекСпрут. Вы узнаете, как использовать официальные зеркала BlackSprut, ссылки на сайт БлекСпрут и способы безопасного доступа через ТОР и VPN. БлекСпрут является одним из наиболее популярных даркнет маркетплейсов, и доступ к нему требует определенных знаний и мер предосторожности.

Что такое БлекСпрут?

БлекСпрут (BlackSprut) – это даркнет маркетплейс, предлагающий широкий ассортимент товаров и услуг. Из-за своей природы и содержания доступ к БлекСпрут осуществляется через сети типа onion, обеспечивающие анонимность пользователей.

Как зайти на БлекСпрут: шаги и инструкции

Шаг 1: Установка ТОР браузера

Первым шагом для доступа к БлекСпрут через ТОР является установка ТОР браузера. Это специализированный браузер, который позволяет анонимно заходить на сайты в onion-сети.

Скачайте ТОР браузер с официального сайта Tor Project.

Установите браузер на ваш компьютер или мобильное устройство.

Запустите ТОР браузер.

Шаг 2: Использование официального зеркала BlackSprut

Для доступа к БлекСпрут важно использовать только проверенные и официальные ссылки. Официальное зеркало BlackSprut гарантирует безопасный доступ и защиту от фишинговых сайтов.

Официальная ссылка на БлекСпрут будет иметь формат.onion. Например, ссылка на сайт БлекСпрут может выглядеть так:

Зеркала сайта БлекСпрут обеспечивают резервный доступ в случае блокировки основного сайта. Например, зеркало БлекСпрут через ТОР:

Шаг 3: Подключение через VPN

Для дополнительной безопасности рекомендуется использовать VPN.

Выберите надежный VPN сервис.

Подключитесь к VPN перед запуском ТОР браузера.

Откройте ТОР браузер и введите официальный адрес БлекСпрут.

Шаг 4: Безопасный доступ к БлекСпрут через onion

Когда вы используете ТОР браузер и официальное зеркало БлекСпрут, важно следовать мерам предосторожности:

Проверяйте URL на наличие ошибок и подлинности.

Используйте VPN для дополнительной защиты.

Не вводите личные данные на подозрительных сайтах.

Часто задаваемые вопросы

Как получить доступ к БлекСпрут через onion?

Для доступа к БлекСпрут через onion сеть необходимо использовать ТОР браузер и официальные ссылки на сайт БлекСпрут. Подключение через VPN также рекомендуется для защиты вашей анонимности.

Как зайти на BlackSprut безопасно?

Чтобы безопасно зайти на BlackSprut, используйте ТОР браузер, подключайтесь через VPN, и проверяйте официальные зеркала сайта БлекСпрут. Никогда не переходите по подозрительным ссылкам.

Что такое зеркало БлекСпрут?

Зеркало БлекСпрут – это альтернативный адрес сайта, используемый для обеспечения доступа в случае блокировки основного сайта. Зеркало BlackSprut через ТОР помогает пользователям получить доступ к маркетплейсу, сохраняя их анонимность.

Теперь вы знаете, как зайти на даркнет маркетплейс БлекСпрут, используя официальные зеркала и ссылки. Следуйте этим инструкциям и соблюдайте меры предосторожности, чтобы обеспечить свою безопасность в даркнете. Официальный сайт BlackSprut и его зеркала через ТОР и VPN помогут вам получить доступ к БлекСпрут, оставаясь анонимным и защищенным.

blacksprutblack sprutссылки бсссылки в бс 2024ссылка на блекспрутрабочая ссылка блекспрутссылки тор блекспрутблекспрут актуальная ссылкаблекспрут ссылка bs0bestтор блекспрутссылки тор блекспрутблекспрут сайтблекспрут официальный сайтблекспрут входкак зайти на блекспруткак зайти на блэкспрутблэкспрут входблэкспрут ссылкаблэкспрут онионблэкспрут даркнетблэкспрут даркнетблэкспрут blacksprut даркнет обзор анонимной даркнет площадкиbs как зайтиbs at как зайти на сайтbs входbs ссылкаblacksprut darknetblacksprutblacksprut зеркалаblacksprut ссылкаblacksprut сайтзеркала blacksprut rusffкак зайти на blacksprutblacksprut официальныйblacksprut com зеркалоblacksprut зеркала онион2fa blacksprutрабочая blacksprutкод blackspruthttps blacksprutкак зайти на blacksprut rusffофициальная ссылка на blacksprutblacksprut маркетплейсрабочее зеркало blacksprutкак зайти на сайт blacksprut2fa код blackspruthttp blacksprutblacksprut bs0best atblacksprut актуальныетор blacksprutblacksprut ссылка rusffbs2best at ссылка blacksprutblacksprut актуальная ссылкаtor blacksprutblacksprut com зеркало rusffhttps blacksprut ссылкаblacksprut зеркала онион rusffblacksprut площадкиbs1site at ссылка blacksprutblacksprut netblacksprut входофициальная ссылка на blacksprut rusffblacksprut blacksprut clickblacksprut bs0tor atblacksprut официальный сайтblacksprut ссылка торкак зайти на сайт blacksprut rusffblacksprut https bs1site atblacksprut http bs0best athttp blacksprut ссылкааккаунты blacksprutрабочее зеркало blacksprut rusffhttps bs2site at ссылка blacksprutbs0best at ссылка blacksprut http bs2best atblacksprut 2blacksprut ссылка blacksprut darknetофициальная ссылка на blacksprutblacksprut ссылка rusffbs0best at ссылка blacksprutblacksprut актуальная ссылкаhttps blacksprut ссылкаbs1site at ссылка blacksprutофициальная ссылка на blacksprut rusffhttp blacksprut ссылкаhttps bs1site at ссылка blacksprutbs0best at ссылка blacksprut http bs0best atblacksprut ссылка tortor blacksprutblacksprut ссылка torblacksprut ссылка tor bs2tor nltor blacksprut rusffblacksprut зеркала torsprutblack sprut

Секреты успешной покупки входной металлической двери, идеально впишется в интерьер.

Места, где можно приобрести качественную входную металлическую дверь.

Как не ошибиться с выбором входной металлической двери.

Почему стоит выбрать металлическую входную дверь.

купить входную дверь заказать входную дверь .

Как выбрать между дверью одного бренда и дверью другого.

Секреты успешной покупки входной металлической двери, которая прослужит долгие годы.

Места, где можно приобрести качественную входную металлическую дверь.

Что учесть при выборе входной металлической двери.

5 основных причин купить металлическую входную дверь.

дверь металлическая входная цена железные двери .

В чем отличия входных металлических дверей разных производителей.

Сколько стоит диплом высшего и среднего образования и как его получить?

стоимость гр золота в скупке где сдать в скупку золото

скупка золота 375 цена скупка золота как изделие спб

Играйте в аркадные игры в лучшем онлайн казино | Играйте в аркадные игры и выигрывайте крупные призы | Победите в аркадах и станьте миллионером | Увлекательные аркадные игры для всех | Онлайн казино с самыми популярными аркадными играми | Азарт и увлечение в аркадном казино | Уникальные аркадные игры ждут вас | Играйте в аркады и выигрывайте деньги | Играйте в аркадные игры и ощутите азарт | Онлайн казино с азартными аркадами | Аркадные игры для всех желающих азарта | Побеждайте в аркадных баталиях и зарабатывайте деньги | Аркадные онлайн развлечения для вас | Новейшие аркадные игры на ваш выбор | Уникальные аркадные игры в онлайн казино | Побеждайте в аркадных играх и получайте призы

arkada casino официальный аркада регистрация .

Лучшее казино для аркадных игр | Погрузитесь в мир азарта и аркадных развлечений | Аркадные игры для всех желающих | Побеждайте в аркадах и получайте крупные денежные призы | Играйте в аркады и наслаждайтесь азартом | Азарт и увлечение в аркадном казино | Азартные аркады для всех желающих | Увлекательные аркады и возможность заработать деньги | Лучшие аркадные развлечения для вас | Аркадные игры и азарт ждут вас в онлайн казино | Играйте в лучшие аркады и выигрывайте призы | Играйте в аркады и выигрывайте крупные суммы | Аркадные онлайн развлечения для вас | Играйте в аркады и получайте удовольствие | Аркадные сражения и азарт для настоящих игроков | Побеждайте в аркадных играх и получайте призы

arkada casino регистрация через телефон arkada casino бонусы за регистрацию .

киного фильмы для компьютера kinogo ретро-фильмы

киного сериалы по популярности киного фильмы по сценаристам

киного спорт киного фильмы про пиратов

киного зарубежные сериалы киного лучшие фильмы по комиксам

киного фильмы для компьютера kinogo фильмы про выживание

киного лучшие триллеры киного зарубежные фильмы

Хотите купить окна окно melke lite по разумной цене? Ознакомьтесь с нашим предложением! У нас — качество, надежность и стиль по доступной стоимости. Индивидуальный подход к каждому заказу!

вызвать шлюх в калуге снять проституток калуга

Хотите купить окна окно melke lite по разумной цене? Ознакомьтесь с нашим предложением! У нас — качество, надежность и стиль по доступной стоимости. Индивидуальный подход к каждому заказу!

дизайнер интерьера квартиры https://dizayn-interera213.ru

шлюхи калуги индивидуалки в калуге

стоимость дизайнера интерьера https://dizayn-interera213.ru

Betzula guncel giris, spor bahisleri konusunda yenilikci cozumler sunar. Fenerbahce Galatasaray derbisi icin betzula guncel giris baglant?s? ile yuksek oranlar? kesfedebilirsiniz.

Betzula’n?n mobil uyumlu tasar?m?, kullan?c?lar?na her zaman kolayl?k saglar. Bet Zula sosyal medya hesaplar?yla yeni kampanyalardan haberdar olabilirsiniz.

en onemli spor etkinliklerinin bahislerinizi an?nda yapabilirsiniz.

Ayr?ca, bet zula giris linki, kullan?c?lara s?n?rs?z erisim sunar. Ozel olarak, bet zula giris, kolay ve h?zl? giris imkan?.

Betzula, en genis bahis seceneklerinden ozel turnuvalara kadar tum kullan?c?lar?n ihtiyaclar?n? kars?lar. en guncel oranlar? gormek icin simdi giris yap?n!

707707+

online slots Jodo Do Tigrinho are a unique combination of excitement and pleasure. Discover a variety of themes, bonus games and jackpots. Play comfortably, enjoying the well-thought-out interface and the chance to hit the jackpot!

Cryptocurrency trading service bitqt with AI is automation and efficiency. Artificial intelligence monitors market dynamics, reduces risks and optimizes transactions. The perfect solution for beginners and professionals.

online slots Jodo Do Tigrinho are a unique combination of excitement and pleasure. Discover a variety of themes, bonus games and jackpots. Play comfortably, enjoying the well-thought-out interface and the chance to hit the jackpot!

Cryptocurrency trading service bitqt with AI is automation and efficiency. Artificial intelligence monitors market dynamics, reduces risks and optimizes transactions. The perfect solution for beginners and professionals.

Спасибо вам!

Представляю вам смотреть мелодраму русскую – это невероятное произведение, которое любят не только в России, но и во всем мире. Они предлагают уникальный взгляд на русскую культуру, историю и обычаи. Сегодня смотреть русские фильмы и сериалы онлайн стало легко благодаря различным платформам и сервисам. От мелодрам до комедий, от исторических лент до современных детективов – выбор огромен. Погрузитесь в захватывающие сюжеты, профессиональную актерскую работу и красивую операторскую работу, наслаждаясь кинематографией из России прямо у себя дома.

доставка алкоголя доставка алкоголя в подольске

доставка алкоголя в бутово доставка алкоголя москва

купить пластиковые окна от производителя окно melke lite

пластиковые окна на балкон цены мелке каталог

киного фильмы для одного киного исторические фильмы

киного фильмы для просмотра дома киного фильмы по алфавиту

kinogo расписание kinogo фильмы с лучшей графикой

киного фильмы для мобильных устройств kinogo фильмы для одного

купить диплом средне специальное образование

Ищете промокоды для игр промо для пополнения баланса ggdrop наш сайт – ваш лучший помощник! Собираем актуальные игровые промокоды для бонусов, скидок и эксклюзивных наград. Наслаждайтесь играми с максимальной выгодой – воспользуйтесь промокодами уже сегодня!

Ищете промокоды для игр промокоды на standoff на кейсы наш сайт – ваш лучший помощник! Собираем актуальные игровые промокоды для бонусов, скидок и эксклюзивных наград. Наслаждайтесь играми с максимальной выгодой – воспользуйтесь промокодами уже сегодня!

Аттестат школы купить официально с упрощенным обучением в Москве

Предлагаем услуги профессиональных инженеров офицальной мастерской.

Еслли вы искали ремонт фотоаппаратов canon цены, можете посмотреть на сайте: ремонт фотоаппаратов canon

Наши мастера оперативно устранят неисправности вашего устройства в сервисе или с выездом на дом!

купить диплом в магадане

фекальный насос фекальный насос .

рыбалка в будни рыбалка на искусственные приманки

аттестат купить в самаре

надежный маркетплейс bs2best at где сочетаются безопасность, широкий выбор товаров и удобство использования. Платформа работает с анонимными платежами и гарантирует полную конфиденциальность для всех пользователей.

катушка для фидера ловля сома ночью

надежный маркетплейс blacksprut где сочетаются безопасность, широкий выбор товаров и удобство использования. Платформа работает с анонимными платежами и гарантирует полную конфиденциальность для всех пользователей.

Как официально приобрести аттестат 11 класса с минимальными затратами времени

buy hash in prague https://shop-cannabis-prague.com

buy weed in prague https://shop-cannabis-prague.com

микрозайм онлайн взять займ онлайн Казахстан

срочно взять деньги под проценты микрокредит

Каждый год выходят новые проекты, которые удивляют зрителей оригинальными сценариями, красивой картинкой и великолепной актерской игрой. Если хочется быть в курсе свежих релизов, стоит заглянуть в раздел дорамы 2025. Здесь можно найти самые ожидаемые новинки, которые обещают покорить сердца поклонников восточных сериалов.

Представляем вам онлайн-портал, с индийскими фильмами и сериалами с онлайн-показом! Здесь вы найдете богатый каталог популярнейших индийских кинолет, а также излюбленные телесериалы, покорившие зрителей во всех странах. Мы представляем различные жанры: от невероятных драм и романтических комедий до мистических триллеров и исторических эпопей. Наша коллекция содержит как классические шедевры, так и новые киноленты, чтобы каждый мог найти что-то подходящее.

Благодаря нашему сайту вы можете посмотреть смотреть индийские фильмы онлайн в хорошем качестве находясь где угодно. Удобный интерфейс и отличное качество видео обеспечивают незабываемый просмотр. Окунитесь в мир болливудского кинематографа и откройте для себя его невероятную культуру вместе с нами!

можно купить аттестат

Нужны деньги срочно взять микрокредит в Казахстане с быстрым одобрением и моментальным переводом на карту. Минимум документов, удобные условия и прозрачные ставки. Оформите займ прямо сейчас!

Промокоды для игр https://esportpromo.com/standoff/ это бесплатные бонусы, скидки и эксклюзивные награды! Находите актуальные коды, используйте их и получайте максимум удовольствия от игры без лишних затрат.

Лучшие игровые промокоды промокод на кейс в одном месте! Активируйте бонусы, получайте подарки и прокачивайте аккаунт без лишних затрат. Следите за обновлениями, чтобы не пропустить новые промо!

Лучшие советы по выбору металлической входной двери, соответствует всем требованиям безопасности.

Лучшие магазины с широким выбором входных металлических дверей.

двери входные металлические москва двери входные металлические москва .

Советы по избежанию ошибок при покупке металлической входной двери.

Преимущества металлических входных дверей перед другими видами.

Сравнение входных металлических дверей различных брендов.

Хотите проверить компанию https://innproverka.ru по ИНН? Наш сервис поможет узнать подробную информацию о юридических лицах и ИП: статус, финансы, руководителей и возможные риски. Защищайте себя от ненадежных партнеров!

Секреты успешной покупки входной металлической двери, идеально впишется в интерьер.

Где купить надежную входную металлическую дверь по выгодной цене.

дверь металлическая заказать двери входные металлические .

Советы по избежанию ошибок при покупке металлической входной двери.

5 основных причин купить металлическую входную дверь.

Сравнение входных металлических дверей различных брендов.

Раскрутка в соцсетях https://nakrytka.com без лишних затрат! Привлекаем реальную аудиторию, повышаем охваты и активность. Эффективные инструменты для роста вашего бренда.

Секреты успешной покупки входной металлической двери, соответствует всем требованиям безопасности.

Лучшие магазины с широким выбором входных металлических дверей.

двери входные металлические москва дверь входная металлическая купить .

Как не ошибиться с выбором входной металлической двери.

Почему стоит выбрать металлическую входную дверь.

Сравнение входных металлических дверей различных брендов.

Легальные способы покупки диплома о среднем полном образовании

[url=https://betano.directorio-de-casinos-mx.com]betano.directorio-de-casinos-mx.com[/url]

Install client casino Betano – win today!

https://www.betano.directorio-de-casinos-mx.com

Логистические услуги в Москве https://bvs-logistica.com доставка, хранение, грузоперевозки. Надежные решения для бизнеса и частных клиентов. Оптимизация маршрутов, складские услуги и полный контроль на всех этапах.

смотреть сериал сезон все серии сериалы смотреть

В 2024 году получить быстрый кредит стало проще. Достаточно выбрать одну из проверенных МФО, отправить заявку и дождаться автоматического одобрения. займ первый без процентов доступны круглосуточно, даже ночью. Это спасение для тех, кому срочно нужны деньги.

Играйте в аркадные игры в лучшем онлайн казино | Играйте в эксклюзивные аркады в онлайн казино | Аркадные игры для всех желающих | Играйте в аркады и выигрывайте деньги | Новый уровень азарта в онлайн казино | Играйте в аркадные игры и выигрывайте деньги | Играйте в аркады и наслаждайтесь выигрышами | Азарт и аркады в одном месте | Аркады и азарт для настоящих игроков | Аркадные игры и азарт ждут вас в онлайн казино | Играйте в лучшие аркады и выигрывайте призы | Побеждайте в аркадных баталиях и зарабатывайте деньги | Испытайте свою удачу в аркадном казино | Аркадные развлечения и азарт вместе | Выигрывайте крупные суммы в аркадных играх | Побеждайте в аркадных играх и получайте призы

arkada casino актуальное зеркало arkada casino играть .

Играйте в аркадные игры в лучшем онлайн казино | Уникальные аркадные игры только здесь | Онлайн казино для ценителей аркадных игр | Увлекательные аркадные игры для всех | Играйте в аркады и наслаждайтесь азартом | Ощутите драйв аркад в онлайн казино | Уникальные аркадные игры ждут вас | Увлекательные аркады и возможность заработать деньги | Аркады и азарт для настоящих игроков | Увлекательные аркады для ценителей азарта | Аркадные игры для всех желающих азарта | Побеждайте в аркадных баталиях и зарабатывайте деньги | Побеждайте в аркадах и станьте миллионером | Увлекательные аркады и возможность заработать крупные суммы | Уникальные аркадные игры в онлайн казино | Побеждайте в аркадных играх и получайте призы

arkada casino онлайн arkada casino бонусы без депозита .

Хотите узнать, какие криптобиржи будут самыми надежными в 2025 году? Мы подготовили для вас подробный обзор топ-10 платформ, которые заслуживают вашего внимания! Узнайте, где лучше торговать, хранить и приумножать свои активы. Читайте статью и выбирайте биржу, которая подходит именно вам!

Биржи с высокой ликвидностью 2025

купить диплом 11 класса

Лучшее казино для аркадных игр | Играйте в эксклюзивные аркады в онлайн казино | Играйте в лучшие аркады на нашем сайте | Увлекательные аркадные игры для всех | Аркадные игры и азарт ждут вас здесь | Ощутите драйв аркад в онлайн казино | Азартные аркады для всех желающих | Самые популярные аркадные игры в одном казино | Играйте в аркадные игры и ощутите азарт | Аркадные игры и азарт ждут вас в онлайн казино | Большие денежные призы в аркадах | Уникальные аркадные игры в вашем распоряжении | Побеждайте в аркадах и станьте миллионером | Новейшие аркадные игры на ваш выбор | Уникальные аркадные игры в онлайн казино | Побеждайте в аркадных играх и получайте призы

зеркало arkada casino casino arkada промокод .

The full special bip39 Word List consists of 2048 words used to protect cryptocurrency wallets. Allows you to create backups and restore access to digital assets. Check out the full list.

Reliable and unique bip39 Word List contains 2048 words needed to create seed phrases in crypto wallets. Allows you to safely manage private keys and guarantees the possibility of recovering funds.

Reliable and unique bip39 Word List contains 2048 words needed to create seed phrases in crypto wallets. Allows you to safely manage private keys and guarantees the possibility of recovering funds.

Как приобрести аттестат о среднем образовании в Москве и других городах

Спасибо за информацию.

Представляю вам смотреть фильмы онлайн бесплатно русские – это настоящее искусство, которое любят не только в России, но и во всем мире. Они раскрывают русскию культуру с новой стороны и рассказывают историю и обычаи. В настоящее время смотреть русские фильмы и сериалы онлайн стало легко за счет множества онлайн кинотеатров. От драм до комедий, от исторических лент до современных детективов – выбор безграничен. Окунитесь в невероятные сюжеты, профессиональную актерскую работу и красивую операторскую работу, смотрите фильмы и сериалы из России не выходя из дома.

The most comprehensive bip39 phrase for securely creating and restoring cryptocurrency wallets. Learn how mnemonic coding works and protect your digital assets!

Prague city moving 777lu.net

The most comprehensive bip39 phrase for securely creating and restoring cryptocurrency wallets. Learn how mnemonic coding works and protect your digital assets!

moving with a guarantee Prague reliable moving companies Prague

The most comprehensive bip39 world list for securely creating and restoring cryptocurrency wallets. Learn how mnemonic coding works and protect your digital assets!

affordable taxi Prague moving personal items Prague

купить диплом программиста

Предлагаем услуги профессиональных инженеров офицальной мастерской.

Еслли вы искали ремонт фотоаппаратов canon рядом, можете посмотреть на сайте: ремонт фотоаппаратов canon

Наши мастера оперативно устранят неисправности вашего устройства в сервисе или с выездом на дом!

Срочно нужны были 25 000 рублей на поездку, но кредитная история испорчена. Друг в WhatsApp скинул ссылку на Новые займы – где найти лучшие предложения , сказал, что там есть компании, которые дают займы онлайн на карту без отказа даже должникам. Подал заявку – одобрили за 2 минуты, деньги получил через 10. Отличный сервис!

Use the proven bip39 world list standard to protect your assets and easily restore access to your finances. A complete list of 2048 mnemonic words used to generate and restore cryptocurrency wallets.

Лучшие решения для автоматизации жалюзи, облегчит вашу жизнь.

Снижайте затраты на отопление и кондиционирование воздуха с автоматизацией жалюзи.

Контролируйте жалюзи с помощью смартфона.

Создайте уютную атмосферу с автоматическими жалюзи.

Качественное обслуживание автоматизированных жалюзи.

жалюзи автоматик https://elektrokarniz18.ru/ .

Современная автоматика для жалюзи, сделает ваш дом уютнее.

Экономьте энергию с помощью автоматики для жалюзи.

Управляйте жалюзи из любой точки мира.

Создайте уютную атмосферу с автоматическими жалюзи.

Опытные специалисты по автоматике для жалюзи.

купить жалюзи с автоматикой https://elektrokarniz18.ru/ .

Полезные советы по покупке диплома о высшем образовании без риска

casino en ligne france 2024 casino en ligne retrait rapide

Full wordlist New full BIP39 2048 words used to create and restore crypto wallets. Multi-language support, high security and ease of use to protect your funds. 2048 mnemonic words for seed generation.

New full Bip39 2048 words used to create and restore crypto wallets. Multi-language support, high security and ease of use to protect your funds.

Лучший выбор для автоматизации жалюзи.

Умное устройство для управления жалюзи.

для коммерческого помещения.

Плюсы использования привода для жалюзи.

Современные разработки для управления жалюзями.

Управление жалюзи через мобильное приложение с использованием привода.

Шаг за шагом по инструкции по установке привода для жалюзи.

Экономьте время и энергию с автоматизированным приводом для жалюзи.

Интересные факты о приводах для жалюзи.

Почему привод для жалюзи делает жизнь легче и удобнее.

жалюзи вентиляционные с ручным приводом жалюзи вентиляционные с ручным приводом .

Идеальный привод для жалюзи.

с использованием привода.

Как выбрать правильный привод для жалюзи.

Преимущества автоматизированного привода для жалюзи.

Тенденции в автоматизации жалюзи с помощью привода.

Как управлять жалюзями с помощью смартфона с использованием привода.

Как установить привод для жалюзи своими руками.

Плюсы привода для жалюзи в экономии ресурсов.

Необычное применение приводов для управления жалюзями.

Секрет уюта и удобства с автоматизированными жалюзями.

привод жалюзи https://elektrokarniz21.ru/ .

Проверенное и надежное казино – selector casino сайт

сколько стоит диплом купить

Предлагаем услуги профессиональных инженеров офицальной мастерской.

Еслли вы искали ремонт фотоаппаратов canon в москве, можете посмотреть на сайте: ремонт фотоаппаратов canon

Наши мастера оперативно устранят неисправности вашего устройства в сервисе или с выездом на дом!

Временная регистрация в Москве – быстро и надежно!

Нужна временная прописка для работы, учебы или оформления

документов? Оформим официальную регистрацию в Москве

всего за 1 день. Без очередей, с гарантией и

юридической чистотой!

? Подходит для граждан РФ и СНГ

? Регистрация от 3 месяцев до 5 лет

? Легально, с внесением в базу МВД

Работаем без предоплаты! Документы можно получить лично или дистанционно.

Доступные цены, оперативное оформление!

Звоните или пишите в WhatsApp прямо сейчас – поможем быстро и

без лишних вопросов!

Временная регистрация в Москве

купить в томске диплом

Необычные электрокарнизы для вашей сцены, подчеркнут красоту представления.

Электрокарнизы – стильное решение для сцены, обеспечивая плавное движение драпировок.

Современные технологии в электрокарнизах, дарят возможность воплотить любую идею.

С электрокарнизами публика останется в восторге, для тех, кто ценит качество и стиль.

Лучшие электрокарнизы для вашего шоу, покоривших сердца зрителей.

Инновационные электрокарнизы для сцены, которые способны изменить восприятие аудитории.

Электрокарнизы – лучший выбор для сцены, с легкой и тихой работой в каждом представлении.

Новейшие электрокарнизы для театральных постановок, способных придать умиротворение или напряжение вашему выступлению.

Электрокарнизы – современное решение для сцены, воплощая самые смелые идеи в жизнь.

Сотни вариантов электрокарнизов для ваших выступлений, чтобы сделать шоу неповторимым и запоминающимся.

карниз для сцены с сенсорным управлением карниз для сцены с сенсорным управлением .

Ваша сцена станет неповторимой с электрокарнизами, подчеркнут красоту представления.

Трансформируйте свою сцену с электрокарнизами, делая представление более динамичным.

Управляйте световыми шоу с помощью электрокарнизов, дарят возможность воплотить любую идею.

С электрокарнизами публика останется в восторге, с идеальным сочетанием функциональности и эстетики.

Электрокарнизы – современное решение для профессиональных выступлений, которые не оставят равнодушными даже самых взыскательных критиков.

Превратите ваше шоу с помощью электрокарнизов, и принести вашему проекту новый уровень.

Уникальные решения для каждого типа представления, которые обеспечат быстрое и плавное движение.

Осуществите свои идеи с помощью электрокарнизов, и подчеркнуть важность каждой сцены.

Обеспечьте шоу непрерывность и слаженность, воплощая самые смелые идеи в жизнь.

Сотни вариантов электрокарнизов для ваших выступлений, чтобы сделать шоу неповторимым и запоминающимся.

лучшие электрокарнизы для театров лучшие электрокарнизы для театров .

купить диплом медицинского образования

[url=https://guru.directorio-de-casinos-mx.com]guru casino[/url]

Install client bookmaker Guru – win today!

http://guru.directorio-de-casinos-mx.com

stehovani s durazem na vybaveni stehovani s moderni technikou

Временная регистрация в Москве – быстро и надежно!

Нужна временная прописка для работы, учебы или оформления документов?

Оформим официальную регистрацию в Москве всего за 1 день. Без очередей,

с гарантией и юридической чистотой!

1. Подходит для граждан РФ и СНГ

2. Регистрация от 3 месяцев до 5 лет

3. Легально, с внесением в базу МВД

Работаем без предоплаты! Документы можно получить лично или дистанционно.

Доступные цены, оперативное оформление!

Звоните или пишите в WhatsApp прямо сейчас – поможем быстро и без лишних вопросов!

Временная регистрация в Москве

вывоз старой мебели в минске грузоперевозки минск

Необычайная автоматизация интерьера с электрокарнизом и таймером, наслаждайтесь комфортом и современностью.

Простота и элегантность в каждой комнате с электрокарнизом и таймером, сделает вашу жизнь проще и приятнее.

Эффективное управление светом и приватностью с электрокарнизом и таймером, современное решение для гармоничного интерьера.

Оптимальное решение для автоматизации штор – электрокарниз с таймером, позволит вам наслаждаться своим временем и пространством.

Инновационные технологии в управлении шторами – электрокарниз с таймером, который сочетает в себе красоту и практичность.

привод для штор умного дома привод для штор умного дома .

Удобное управление шторами с помощью электрокарниза и таймера, наслаждайтесь комфортом и современностью.

Простота и элегантность в каждой комнате с электрокарнизом и таймером, сделает вашу жизнь проще и приятнее.

Освободите руки и ум с электрокарнизом и таймером, для вашего удобства и удовольствия.

Умное устройство для вашего дома – электрокарниз с таймером, обеспечит вас и вашу семью уютом и функциональностью.

Инновационные технологии в управлении шторами – электрокарниз с таймером, позволит вам экономить время и силы.

умные рулонные шторы на пластиковые окна https://prokarniz50.ru/ .

Pretty! This was an incredibly wonderful article. Many thanks for providing this info.

официальный сайт lee bet

Howdy! I’m at work surfing around your blog from my new iphone 4! Just wanted to say I love reading your blog and look forward to all your posts! Keep up the great work!

вход банзай бет

Каталог финансовых организаций https://srochno-zaym-online.ru в которых можно получить срочные онлайн займы и кредиты не выходя из дома через интернет.

WOW just what I was looking for. Came here by searching for %keyword%

регистрация драгон мани

hdrezka субтитры hd rezka фильмы ужасы 1080p бесплатно

Каталог финансовых организаций https://srochno-zaym-online.ru в которых можно получить срочные онлайн займы и кредиты не выходя из дома.

квартирный переезд из минска в гродно грузоперевозки минск

бесплатный доступ к кино в хорошем качестве hdrezka фэнтези hd на телевизоре

Каталог финансовых организаций srochno-zaym-online.ru в которых можно получить срочные онлайн займы и кредиты не выходя из дома.

Создайте идеальную атмосферу в вашем доме с программируемым электрокарнизом, совместим с любым интерьером.

Превратите свой дом в оазис комфорта с программируемым электрокарнизом, который дарит вам полный контроль.

Сделайте вашу жизнь проще с программируемым электрокарнизом, поможет вам создать идеальный микроклимат.

Пусть ваша спальня станет местом для отдыха и релаксации с программируемым электрокарнизом, создаст идеальную атмосферу для полноценного отдыха.

Регулируйте интенсивность света и тепла с помощью программируемого электрокарниза, который сделает вашу жизнь проще и комфортнее.

как подключить электрокарниз к умному дому как подключить электрокарниз к умному дому .

лучшие американские сериалы онлайн фильмы hdrezka на телевизоре

Управляйте своим окружением с помощью программируемого электрокарниза, совместим с любым интерьером.

Создайте идеальное освещение в вашем доме с программируемым электрокарнизом, который дарит вам полный контроль.

Сделайте вашу жизнь проще с программируемым электрокарнизом, поможет вам создать идеальный микроклимат.

Пусть ваша спальня станет местом для отдыха и релаксации с программируемым электрокарнизом, создаст идеальную атмосферу для полноценного отдыха.

Управляйте светом и теплом в вашем доме с программируемым электрокарнизом, обеспечит вас уютом и спокойствием.

умный электрокарниз xiaomi умный электрокарниз xiaomi .

best smm panel boost subscribers boost of subscribers in tik tok

Идеи вашего дома. Информация о дизайне и архитектуре.

Syndyk – это место, где каждый день вы можете увидеть много различных дизайнерских решений, деталей для вашей квартиры, проектов домов, лучшая сантехника.

Если вы дизайнер или архитектор, то мы с радостью разместим ваш проект на Сундуке. На сайте можно и даже нужно обмениваться мнениями и информацией о дизайне и архитектуре.

Сайт: syndyk.by

Идеи вашего дома. Информация о дизайне и архитектуре.

Syndyk – это место, где каждый день вы можете увидеть много различных дизайнерских решений, деталей для вашей квартиры, проектов домов, лучшая сантехника.

Если вы дизайнер или архитектор, то мы с радостью разместим ваш проект на Сундуке. На сайте можно и даже нужно обмениваться мнениями и информацией о дизайне и архитектуре.

Сайт: syndyk.by

Всё о строительстве, дизайне и ремонте в своём доме.

Что вы найдете на нашем сайте?

Экспертные советы

Статьи разработаны профессионалами в области строительства, дизайна и ремонта.

Полезные ресурсы

Ссылки на проверенные магазины, услуги и материалы, которые помогут вам в ваших проектах.

Модные тренды

Мы следим за последними тенденциями и новинками в мире строительства и дизайна.

«Свой Угол» – ваш проводник в мире уюта и стиля в вашем доме. Погружайтесь в наши статьи, найдите вдохновение, задавайте вопросы и делитесь своим опытом.

Создайте свой угол вместе с нами!

Информационный портал svoyugol.by

Предлагаем услуги профессиональных инженеров офицальной мастерской.

Еслли вы искали ремонт iphone 11, можете посмотреть на сайте: ремонт iphone 11 в москве

Наши мастера оперативно устранят неисправности вашего устройства в сервисе или с выездом на дом!

Предлагаем услуги профессиональных инженеров офицальной мастерской.

Еслли вы искали ремонт iphone 11 в москве, можете посмотреть на сайте: ремонт iphone 11

Наши мастера оперативно устранят неисправности вашего устройства в сервисе или с выездом на дом!

Кодирование от алкоголизма в Барнауле в частной клинике «Рехаб22» – это эффективное и анонимное лечение с гарантией результата. rehab-22

купить exalted orbs poe 2 poe 2 прокачка персонажа

https://copychief.com/art/888starz-promo-code.html

https://jnp.chitkara.edu.in/pages/articles/c_digo_promocional_67.html

секс порно чат

секс порно чат пары порно чат онлайн пары

русский порно чат

секс чат онлайн онлайн эро чат пары

https://playplayfun.com/articles/1xbet_promo_code_nigeria_bonus.html

The promo code for 1XBET is “1XBUM.” By utilizing this code, you can unlock a special bonus for sports betting, offering a 100% match up to $130, or for casino games, a bonus of $1,950 along with 150 free spins. New players have the opportunity to input our 1xBet bonus code to enhance the standard sports free bet bonus by an additional $100. A 1xBet promo code consists of a combination of letters and numbers that you enter in a designated voucher field to access these advantageous offers.

1xbet ar promo code

The promo code for 1XBET is “1XBUM.” By utilizing this code, you can unlock a special bonus for sports betting, offering a 100% match up to $130, or for casino games, a bonus of $1,950 along with 150 free spins. New players have the opportunity to input our 1xBet bonus code to enhance the standard sports free bet bonus by an additional $100. A 1xBet promo code consists of a combination of letters and numbers that you enter in a designated voucher field to access these advantageous offers.

1xbet promo code in somalia

https://www.u-ma.co.jp/pag/?paripesa_promo_code.html

Лучший выбор для автоматизации жалюзи.

Умное устройство для управления жалюзи.

Секреты выбора привода для жалюзи.

Преимущества автоматизированного привода для жалюзи.

Инновационные технологии в области приводов для жалюзи.

Как управлять жалюзями с помощью смартфона с использованием привода.

Секреты успешной установки привода для автоматизации жалюзей.

Почему стоит выбрать привод для автоматизации жалюзей.

Забавные истории об использовании приводов для жалюзей.

Секрет уюта и удобства с автоматизированными жалюзями.

умный привод жалюзи умный привод жалюзи .

Лучший выбор для автоматизации жалюзи.

Эффективное решение для автоматизации жалюзей.

для офиса.

Преимущества автоматизированного привода для жалюзи.

Современные разработки для управления жалюзями.

Простой способ контролировать жалюзи с телефона с использованием привода.

Секреты успешной установки привода для автоматизации жалюзей.

Плюсы привода для жалюзи в экономии ресурсов.

Забавные истории об использовании приводов для жалюзей.

Почему привод для жалюзи делает жизнь легче и удобнее.

привод жалюзи вентиляции https://elektrokarniz21.ru/ .

для коммерческого помещения.

с помощью привода.

для коммерческого помещения.

Зачем нужен привод для автоматизации жалюзей.

Современные разработки для управления жалюзями.

Как управлять жалюзями с помощью смартфона с использованием привода.

Шаг за шагом по инструкции по установке привода для жалюзи.

Экономьте время и энергию с автоматизированным приводом для жалюзи.

Забавные истории об использовании приводов для жалюзей.

Секрет уюта и удобства с автоматизированными жалюзями.

жалюзи с приводом на окна жалюзи с приводом на окна .

Либет Казино – это новый уровень онлайн развлечений! Регистрируйтесь на нашем сайте уже сейчас и погружайтесь в мир азарта вместе с Либет Казино! leebet casino сайт

порно чат онлайн пары эро чат

Управляйте своим окружением с помощью программируемого электрокарниза, подходит для любого окна.

Создайте идеальное освещение в вашем доме с программируемым электрокарнизом, позволяет вам наслаждаться каждой минутой.

Освежите свою обстановку с помощью программируемого электрокарниза, который позволит вам сохранить энергию.

Превратите свою спальню в уютное убежище с программируемым электрокарнизом, дарит вам возможность наслаждаться каждой минутой вашего сна.

Управляйте светом и теплом в вашем доме с программируемым электрокарнизом, поможет вам сэкономить время и энергию.

как подключить электрокарниз к умному дому как подключить электрокарниз к умному дому .

игровые автоматы топ casino

рейтинг игровых автоматов онлайн по выплатам легальные игровые автоматы онлайн

Управляйте своим окружением с помощью программируемого электрокарниза, совместим с любым интерьером.

Трансформируйте ваше жилище с помощью программируемого электрокарниза, который дарит вам полный контроль.

Пусть ваш дом всегда выглядит стильно и современно с программируемым электрокарнизом, обеспечит вам максимальный комфорт.

Пусть ваша спальня станет местом для отдыха и релаксации с программируемым электрокарнизом, создаст идеальную атмосферу для полноценного отдыха.

Создайте идеальные условия для работы и отдыха с программируемым электрокарнизом, поможет вам сэкономить время и энергию.

умный электрокарниз для штор https://elektrokarniz190.ru/ .

Управляйте своим окружением с помощью программируемого электрокарниза, совместим с любым интерьером.

Трансформируйте ваше жилище с помощью программируемого электрокарниза, позволяет вам наслаждаться каждой минутой.

Освежите свою обстановку с помощью программируемого электрокарниза, который позволит вам сохранить энергию.

Создайте идеальные условия для сна с помощью программируемого электрокарниза, который поможет вам легко заснуть и проснуться.

Управляйте светом и теплом в вашем доме с программируемым электрокарнизом, который сделает вашу жизнь проще и комфортнее.

электрокарниз подключение к умному дому https://elektrokarniz190.ru/ .

kinogo рейтинги kinogo дублированные фильмы

киного лучшие фильмы киного фильмы для отдыха

https://bonk24.com/

https://actual-cosmetology.ru/pgs/1xbet_promokod_pri_registracii_na_segodnya_besplatno.html

Excellent write-up. I definitely appreciate this site.

Stick with it!

MUSICBR.RU — сайт о том, как научиться играть на гитаре с нуля.

Здесь вы найдете видеоуроки и разборы песен на гитаре,

рифмованные (эквиритмические) переводы песен на русском,

а также советы и рекомендации от автора канала «Музыкант вещает» на YouTube.

Сайт musicbr.ru

Тут можно преобрести сейф оружейный цена оружейные шкафы

Тут можно преобрести несгораемые сейфы огнестойкий сейф купить

Тут можно преобрести купить сейф огнестойкий сейф несгораемый

Необычайная автоматизация интерьера с электрокарнизом и таймером, наслаждайтесь комфортом и современностью.

Создайте атмосферу уюта и стиля с помощью электрокарниза и таймера, добавит функциональности и комфорта.

Освободите руки и ум с электрокарнизом и таймером, современное решение для гармоничного интерьера.

Умное устройство для вашего дома – электрокарниз с таймером, который упростит вашу жизнь и сделает ее более комфортной.

Дизайнерское решение для современного дома – электрокарниз с таймером, который сочетает в себе красоту и практичность.

умный дом рулонные шторы умный дом рулонные шторы .

http://centroculturalrecoleta.org/blog/pages/chizkeyk_s_rikottoy_po_italyyanski.html

купить диплом в вологде

Удобное управление шторами с помощью электрокарниза и таймера, экономьте энергию и время.

Создайте атмосферу уюта и стиля с помощью электрокарниза и таймера, который подчеркнет ваш вкус и индивидуальность.

Освободите руки и ум с электрокарнизом и таймером, современное решение для гармоничного интерьера.

Оптимальное решение для автоматизации штор – электрокарниз с таймером, который упростит вашу жизнь и сделает ее более комфортной.

Дизайнерское решение для современного дома – электрокарниз с таймером, добавит функциональности и удобства в вашу жизнь.

умные оконные шторы умные оконные шторы .

Удобное управление шторами с помощью электрокарниза и таймера, наслаждайтесь комфортом и современностью.

Создайте атмосферу уюта и стиля с помощью электрокарниза и таймера, добавит функциональности и комфорта.

Эффективное управление светом и приватностью с электрокарнизом и таймером, для вашего удобства и удовольствия.

Оптимальное решение для автоматизации штор – электрокарниз с таймером, обеспечит вас и вашу семью уютом и функциональностью.

Инновационные технологии в управлении шторами – электрокарниз с таймером, позволит вам экономить время и силы.

Автоматический карниз для штор https://prokarniz50.ru/ .

Whoa quite a lot of amazing info.

miami slots online casino https://usagamblingexperts.com/fast-payout-casino/ best online cash casino

seattle seo agency source

buy pet products order pet product

best pet products pet store

Здесь можно сейф купить в москве сейф

Тут можно преобрести навесы металлические в Санкт-Петербурге подробно на сайте навес для машин

Тут можно преобрести шкаф для оружия цена купить сейф для охотничьего карабина

Тут можно преобрести металлический навес в Санкт-Петербурге подробно на сайте навес на дачу

купить диплом онлайн купить диплом онлайн .

Hey! I understand this is kind of off-topic however I needed to ask.

Does building a well-established website such as yours take a lot

of work? I am completely new to running a blog but I do write in my journal on a daily basis.

I’d like to start a blog so I can easily share my experience and thoughts online.

Please let me know if you have any kind of ideas or

tips for new aspiring bloggers. Appreciate it!

Тут можно преобрести купить сейф взломостойкий взломостойкие сейфы купить

Тут можно преобрести сейфы офисные цены сейф для офиса купить москва

Тут можно преобрести купить сейф офисный сейф офисный для денег

Необычные электрокарнизы для вашей сцены, которые удивят зрителей.

Электрокарнизы – стильное решение для сцены, делая представление более динамичным.

Управляйте световыми шоу с помощью электрокарнизов, дарят возможность воплотить любую идею.

Электрокарнизы помогут создать атмосферу шоу, с идеальным сочетанием функциональности и эстетики.

Лучшие электрокарнизы для вашего шоу, с непревзойденным качеством и надежностью.

Сверхсовременные технологии в каждом дизайне, сделать ваше выступление неповторимым.

Освежите свое шоу с электрокарнизами, и создадут неповторимую атмосферу.

С электрокарнизами ваша сцена станет настоящим шедевром, способных придать умиротворение или напряжение вашему выступлению.

Обеспечьте шоу непрерывность и слаженность, с индивидуальным подходом к каждому проекту.

Выберите электрокарнизы по своему вкусу, чтобы сделать шоу неповторимым и запоминающимся.

монтаж электрокарниза в театре https://elektrokarniz8.ru/ .

Лучшие электрокарнизы для профессиональной сцены, которые удивят зрителей.

Электрокарнизы – стильное решение для сцены, позволяя создать эффектные декорации.

Электрокарнизы для сцены с электронным управлением, дарят возможность воплотить любую идею.

Электрокарнизы помогут создать атмосферу шоу, с идеальным сочетанием функциональности и эстетики.

Электрокарнизы – современное решение для профессиональных выступлений, с непревзойденным качеством и надежностью.

Сверхсовременные технологии в каждом дизайне, сделать ваше выступление неповторимым.

Уникальные решения для каждого типа представления, которые обеспечат быстрое и плавное движение.

Новейшие электрокарнизы для театральных постановок, способных придать умиротворение или напряжение вашему выступлению.

Трансформируйте свой спектакль с электрокарнизами, воплощая самые смелые идеи в жизнь.

Выберите электрокарнизы по своему вкусу, и удивить зрителей нестандартными решениями.

рейтинг электрокарнизов для сцены рейтинг электрокарнизов для сцены .

Лучшие электрокарнизы для профессиональной сцены, которые удивят зрителей.

Электрокарнизы придают шоу утонченность, обеспечивая плавное движение драпировок.

Управляйте световыми шоу с помощью электрокарнизов, которые делают шоу невероятно красивым.

Электрокарнизы помогут создать атмосферу шоу, где каждая деталь важна.

Электрокарнизы – современное решение для профессиональных выступлений, с непревзойденным качеством и надежностью.

Сверхсовременные технологии в каждом дизайне, сделать ваше выступление неповторимым.

Освежите свое шоу с электрокарнизами, и создадут неповторимую атмосферу.

Новейшие электрокарнизы для театральных постановок, для тех, кто стремится к совершенству.

Трансформируйте свой спектакль с электрокарнизами, с индивидуальным подходом к каждому проекту.

Выберите электрокарнизы по своему вкусу, чтобы сделать шоу неповторимым и запоминающимся.

как выбрать электрокарниз для театра как выбрать электрокарниз для театра .